If you're dealing with cold drafts in January, hot upstairs rooms in July, or windows that rattle every time the wind picks up, you're probably already asking the main question. Not whether you need new windows, but how to pay for them without wrecking your budget.

That's the right question. In Boise, window replacement is a meaningful home upgrade, not a small weekend expense. The smart move is to look at the full project economics. That means the window package, the financing term, any rebate you can qualify for, and whether a city program can lower your cost even more. Monthly payment matters, but it's not the whole story.

A lot of homeowners focus too narrowly on “Can I get approved?” I think that's backwards. Start with “What structure makes this project affordable and still gets me the performance I want?” That's how you make good decisions on window financing in Boise, Idaho.

Table of Contents

- Why Boise Homeowners Consider Financing New Windows

- Your Primary Window Financing Options Explained

- The Financing Application Process Demystified

- Unlocking Boise-Area Rebates and Public Programs

- Choosing Terms Wisely and Avoiding Common Pitfalls

- Take the Next Step to a More Comfortable Home

Why Boise Homeowners Consider Financing New Windows

Homeowners don't wake up wanting a financing plan. They wake up annoyed by failing windows.

It's the bedroom that never holds temperature. The living room glass that feels cold when you sit nearby. The summer cooling bill that reminds you your old units are leaking comfort all day long. If that sounds familiar, financing isn't some last resort. It's a practical way to solve a house problem now instead of stretching it out for another few seasons.

The numbers make that clear. Contractor Plus estimates the 2026 cost to replace windows in Boise, Idaho at $5,686.35 to $11,372.69, including materials and professional labor, and notes that final pricing depends on project scope, material quality, labor, access, permits, inspections, debris removal, and structural modifications, as shown in its Boise window replacement cost projection. That's squarely in the range where many homeowners prefer installment plans over paying the entire amount at once.

Financing is often the sensible choice

For a single window, paying cash may be easy. For a whole-home project, it's a different conversation.

Financing gives you options:

- Protect your cash reserves: Keep savings available for emergencies or other home repairs.

- Replace all problem windows at once: Avoid piecemeal work that leaves the house uneven in comfort and appearance.

- Choose better glass packages upfront: Better efficiency usually costs more at installation, but it can improve comfort from day one.

Practical rule: If your windows are affecting comfort in multiple rooms, don't let “I'll wait and save up” turn into another year of poor performance.

A lot of Boise homeowners also tie the purchase to utility savings and year-round comfort. If you want a deeper look at that side of the equation, this guide on whether new windows save money on heating bills in Idaho is worth reading.

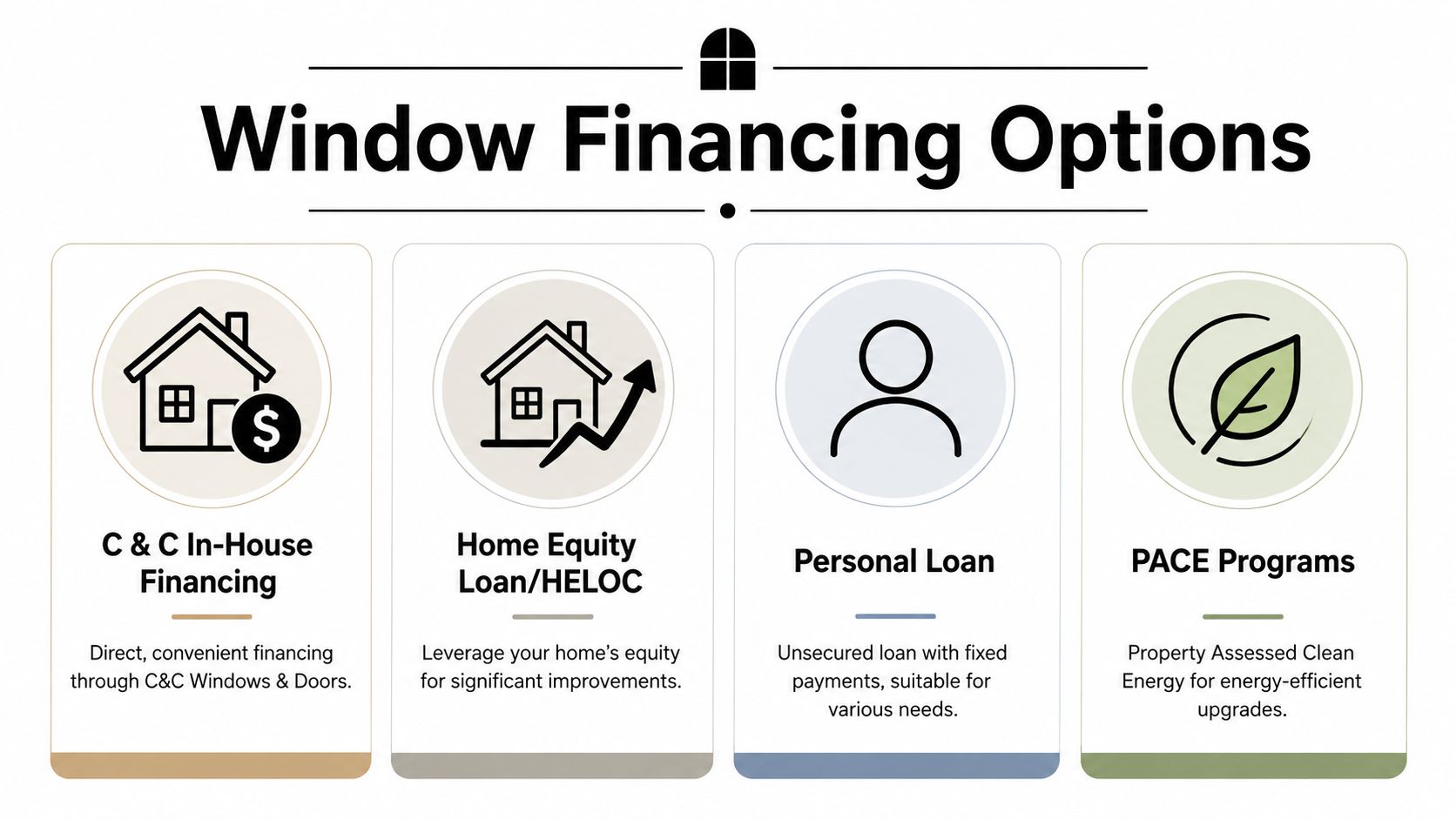

Your Primary Window Financing Options Explained

Window financing in Boise, Idaho usually falls into a few buckets. Promotional financing, fixed-term installment loans, home equity borrowing, and general personal lending. Each can work. Each also has a catch if you choose based only on the monthly payment.

The first thing I tell homeowners is simple. Don't compare financing by payment alone. Compare by structure. The same project can feel easy or expensive depending on term length, rate, and whether a promo period fits your payoff plan.

Why term length changes the deal

One industry financing guide shows how dramatically terms can shift the payment. It cites a 12-month same-as-cash option, a 60-month loan at about 6.99% APR, and a 180-month loan at about 11.99% APR, with example payments of roughly $290 per month and $174 per month on a sample project, as outlined in this window and door financing term example.

That's the tradeoff in plain English. A longer term lowers the monthly burden. It also means you carry the project much longer and typically pay more in finance charges over time.

Financing term comparison

Here's a simple side-by-side view of how homeowners usually think through it.

| Financing Option | Example APR | Estimated Monthly Payment | Best For |

|---|---|---|---|

| Same-as-cash promotional plan | Promotional | Varies by payoff timing | Homeowners who can pay the balance during the promo window |

| Fixed loan over 60 months | About 6.99% | Roughly $290/month | Owners who want a shorter payoff and more controlled total borrowing cost |

| Fixed loan over 180 months | About 11.99% | Roughly $174/month | Households prioritizing lower monthly cash flow |

| Home equity loan or HELOC | Varies | Varies | Larger projects where the owner wants to use home equity |

If you're still sorting out project size before choosing a term, start with a realistic scope. This breakdown of how much window replacement costs in Boise, Idaho can help you frame the budget correctly.

Which option fits which homeowner

A short promotional term works well for disciplined borrowers. If you know a bonus, tax refund, or other planned cash event will let you pay it off during the promotional period, this can be efficient. If you're guessing, be careful.

A medium-term fixed loan is usually the most balanced path. The payment is higher than a long loan, but the project doesn't linger on your budget forever.

A long-term loan can make a full-house replacement possible when cash flow is tight. That matters for many households. Just go into it with clear eyes. Lower payment does not mean lower cost.

Some local installers also offer retail financing through lending partners. For example, C & C Windows & Doors offers financing through Synchrony for window and patio door projects. That can simplify the process because estimate, product selection, and financing review happen in the same workflow.

Choose the shortest term that still leaves your monthly budget comfortable. That's usually the sweet spot.

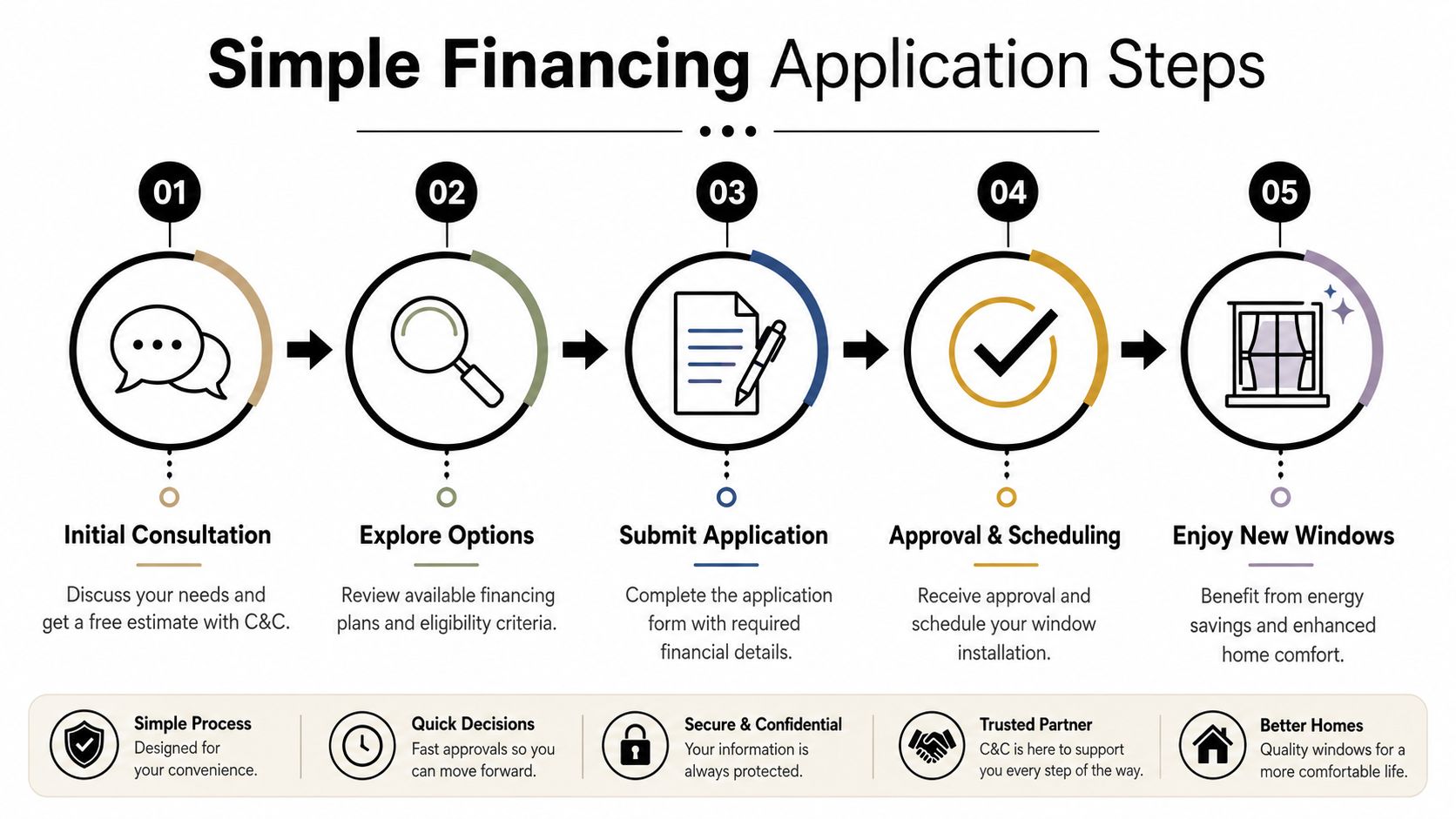

The Financing Application Process Demystified

The application process worries people more than it should. In practice, it's usually a short sequence: confirm project scope, review options, submit an application, then schedule installation after approval.

What slows people down isn't complexity. It's not having the right information ready.

What usually happens first

The first step is the home consultation and estimate. That matters because lenders and financing programs work from an actual project amount, not a rough guess you came up with online.

During that visit, you want clear answers on:

- Scope: Are you replacing every window or just the worst ones?

- Product level: Standard double-pane, upgraded glass package, or triple-pane.

- Installation factors: Any access issues, trim work, or structural corrections that may affect final pricing.

Once you know the complete scope, the financing conversation gets easier. You're no longer shopping blind.

What to have ready

Most financing applications move faster when you gather the basics ahead of time. The exact list can vary by lender, but homeowners are usually asked for standard identity and financial details.

Bring or prepare:

- Government-issued identification: So the lender can verify the applicant.

- Income information: This helps support repayment review.

- Property details: Address, ownership status, and project location.

- Project estimate: The lender needs to know what is being financed.

A clean application starts with a clean estimate. If the project scope keeps changing, the financing process usually gets messier too.

If two owners are on title, it's smart to decide early who will apply and whether the application should include both parties. That avoids delays, duplicate paperwork, and confusion later when the installation is ready to schedule.

What approval really means

Approval isn't the finish line. It means the financial side is lined up well enough to move forward.

You still need to confirm the details that affect the homeowner experience:

- Promotional period rules: Know exactly when the special terms end.

- Monthly payment expectations: Make sure the number fits your real budget, not your optimistic budget.

- Project timing: Ask when materials are ordered and how scheduling works after documents are signed.

This is also the point where smart homeowners ask one more question. “Are there any rebate or public program requirements I need to satisfy before installation?” That question can save you money and headaches.

Unlocking Boise-Area Rebates and Public Programs

A Boise homeowner finances new windows at a comfortable monthly payment, then finds out later the chosen glass package missed a utility rebate by a small margin. I see that mistake all the time, and it costs real money.

The right way to handle this part of the project is to look at total cost first. Your financing, utility incentives, tax credit potential, and any public assistance options should all work together before the order is placed.

Utility rebates favor homeowners who plan early

Rebate money usually goes to the homeowners who ask better questions before installation, not after it.

According to this Idaho utility efficiency program overview, Idaho utilities may tie rebates or special financing to specific performance standards, pre-approval steps, inspections, and required documentation. In practical terms, that means your window package, contractor paperwork, and project timing all matter.

For Boise-area homes, start with these checks before you sign:

- Does your utility offer a current rebate for window replacement?

- Does the window package meet the required U-factor or other efficiency standard?

- Do you need approval before materials are ordered or work begins?

- What paperwork must you keep after installation?

- How fast do you need to submit the rebate claim?

If you skip those questions, you can still end up with good windows. You just may miss the savings that would have improved the whole project math.

Public programs can change the budget more than the financing term

For some Boise homeowners, the bigger opportunity is not shaving a few dollars off the monthly payment. It is qualifying for help that lowers the actual project cost or gives you access to a lower-rate structure.

The City of Boise offers a Home Improvement Program that can include window and door work, along with other eligible repairs and energy-efficiency improvements for qualifying homeowners. If you are reviewing the full incentive picture, this guide to the window replacement tax credit in Idaho for 2026 is also worth reading alongside utility and city programs.

That combination matters. A homeowner who qualifies for assistance, claims available incentives, and finances only the remaining balance is usually in a stronger position than someone who focuses only on the first loan offer.

Build the project around net cost

Here is the order I recommend for Treasure Valley homeowners:

- Check utility and public-program eligibility first.

- Choose the window package to meet comfort goals and any rebate requirements.

- Calculate the net project cost after incentives and credits you reasonably expect to receive.

- Finance the remaining amount with terms that fit your actual monthly budget.

- Save every invoice, spec sheet, and approval email in one folder.

The lowest payment does not always produce the lowest project cost. In Boise, the better financial move is often the one that combines the right window performance with every rebate, credit, and program you can use.

Choosing Terms Wisely and Avoiding Common Pitfalls

Boise homeowners make the same mistake every year. They shop for the lowest monthly payment first, then back into the product choice.

I'd flip that every time. Choose the right window performance for your house, then choose the financing term that lets you carry it responsibly.

Buy for performance, not just payment

Independent financing guidance notes that replacement windows commonly cost about $500 to $700 per window on average in the U.S., with a broader range of $200 to $1,500 per window depending on specifications, and it points out that financing can make higher-performance options such as triple-pane glass and lower-U-factor packages more accessible upfront, as explained in this window financing and performance guide.

That matters in Boise. If your house gets full afternoon sun, if certain rooms are always uncomfortable, or if you're trying to reduce outside noise, higher-performance glass can be a better use of financing than a bare-minimum product.

Mistakes that cost homeowners money

I see a few avoidable errors again and again.

- Chasing the lowest payment: A small monthly number can hide a long repayment period and a bigger total cost.

- Ignoring promo deadlines: Same-as-cash can work well, but only if you clear the balance on time.

- Underbuying the window package: Homeowners sometimes finance a cheaper unit, then regret the missed comfort and efficiency benefits.

- Forgetting project extras: Trim, access issues, structural corrections, and permit-related items can affect the final budget.

- Missing rebate requirements: A technically nonqualifying window can wipe out a rebate opportunity.

Here's my opinion. If you're going to finance at all, use it to buy the window you want to live with for years. Don't stretch out payments on a weak product just because the monthly number feels easier.

A good financing decision does three things at once. It keeps your payment manageable, gets you the performance your home needs, and preserves flexibility in your monthly budget.

Take the Next Step to a More Comfortable Home

You get the winter bill, hear traffic through the bedroom window again, and still have one sash that sticks every time you try to open it. At that point, waiting is rarely the cheaper choice. It usually means more discomfort, another season of weak performance, and a rushed decision later.

Here's the right way to handle it in Boise. Price the whole project for your house, then compare the complete financial picture. That means window scope, installation details, energy-performance specs, financing terms, utility rebates, and any public assistance you may qualify for.

As noted earlier, some Boise homeowners may qualify for city home improvement help that can include window work. If that applies to your household, put that option on the table first. If it does not, build the project around private financing and any Idaho Power or Avista rebate your window package can support.

That is the part too many homeowners miss. A lower monthly payment does not automatically mean a better deal. A better deal is the one that fits your budget, keeps total borrowing cost under control, and gets you windows that solve the comfort, noise, and efficiency problems you face.

Start with three numbers:

- The installed project cost

- The rebate or assistance dollars you can realistically apply

- The total repayment cost over the term you are considering

Then make your decision.

Do not approve a project based on a teaser payment. Do not assume every window package qualifies for incentives. Do not finance a stripped-down option if you already know your home needs better glass performance for sun exposure, street noise, or draft control.

Get the scope right first. Then choose financing that supports the full value of the project.

Schedule a free in-home consultation with C & C Windows & Doors if you want a clear project plan for your Treasure Valley home. You'll be able to review window options, get a same-day estimate, and talk through financing in practical terms so you can choose a structure that fits your budget and your long-term comfort goals.